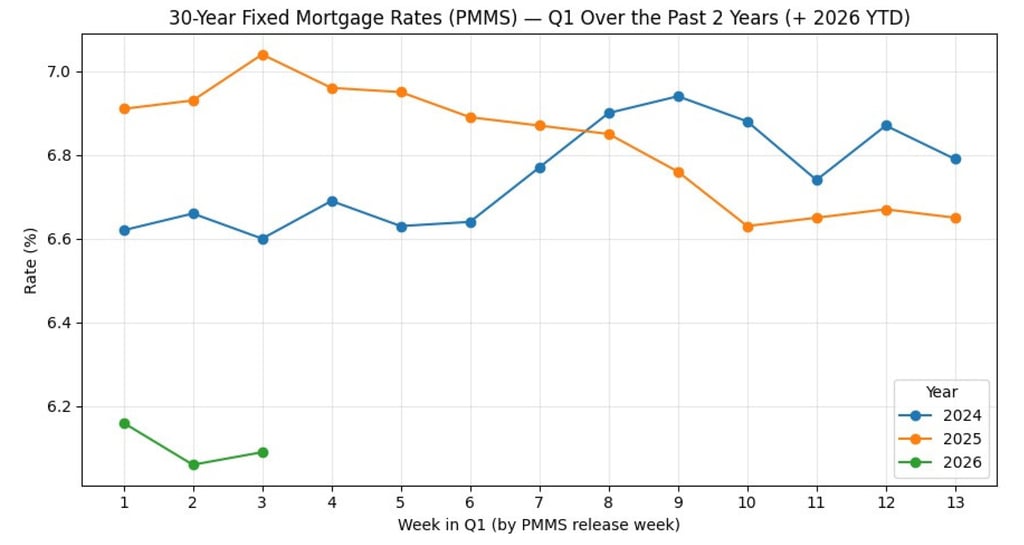

The mortgage market entered 2026 on a noticeably calmer note, with average 30-year rates starting the year roughly 1% lower than where they stood a year ago—an important shift that’s changing how buyers and homeowners approach the market.

The Mortgage Market Is Calming Down — And That’s Actually Good News

If the mortgage market felt a little unpredictable over the past year, you weren’t imagining it. Rates moved fast, headlines moved faster, and a lot of buyers hit pause waiting for the “perfect moment.”

Here’s the good news: the market is starting to act a lot more like a grown-up.

As we move into 2026, mortgage conditions are becoming more predictable, home price growth is stabilizing, and opportunities are opening up for buyers and homeowners who understand how to navigate the landscape.

And no — this isn’t about chasing the lowest rate.

What Happened in the Fourth Quarter?

The fourth quarter marked an important shift. After months of volatility, mortgage rates stopped swinging wildly and settled into a more consistent range. While rates are still higher than the historic lows of years past, the chaos cooled off — and that matters more than people realize.

Stability builds confidence.

Confidence gets deals done.

Buyers who succeeded late last year weren’t waiting for perfection. They focused on smart financing strategies, realistic monthly payments, and long-term affordability. That mindset made all the difference.

Why Stability Matters More Than Headlines

When rates move sharply, buyers freeze. When rates stabilize, buyers plan.

That’s exactly what we saw toward the end of the year. Instead of reacting to every rate headline, buyers began asking better questions:

What does this payment look like long-term?

How can seller concessions help?

Are there creative ways to structure this loan?

Those are the questions that lead to homeownership — even in higher-rate environments.

What We’re Watching as We Enter the First Quarter

Early indicators suggest mortgage rates are likely to remain within a relatively narrow range rather than bouncing dramatically up or down. Even small improvements can bring buyers off the sidelines quickly, especially first-time and move-up buyers who have been waiting for more certainty.

Inventory remains limited, which continues to support home values. At the same time, buyers are more payment-conscious than ever. Price growth has slowed compared to recent years, giving well-prepared buyers more room to strategize instead of rush.

In today’s market, preparation beats timing.

Homeowners: This Part Is Especially for You

If you already own a home, this environment presents an opportunity that’s easy to overlook.

Many homeowners are sitting on significant equity. That equity can sometimes be used in creative ways to:

And no — this doesn’t require waiting for dramatic rate drops.

A simple mortgage review can uncover options that weren’t available when you first bought or refinanced. Sometimes small adjustments can create meaningful long-term benefits.

The Bottom Line

The mortgage market isn’t perfect — but it’s calmer, clearer, and more workable than it’s been in a while. Buyers who focus on strategy instead of headlines are finding success. Homeowners who take time to review their options may discover opportunities hiding in plain sight.